|

|

| Mutual Fund |

| |

|

|

|

Mutual Funds are financial instruments. These funds are collective investments which gather money from different investors to invest in stocks, short-term money market financial instruments, bonds and other securities and distribute the proceeds as dividends. The Mutual Funds in India are handled by Fund Managers, also referred as the portfolio managers. The Securities Exchange Board of India regulates the Mutual Funds in India. The unit value of the Mutual Funds in India is known as net asset value per share (NAV). The NAV is calculated on the total amount of the Mutual Funds in India, by dividing it with the number of units issued and outstanding units on daily basis.

|

|

Benefits of Investing in Mutual Funds

Any one who is aware of stock market is not new to mutual funds. Mutual funds have gained in popularity with the investing public especially in the last two decades.Following are some of the primary benefits.

|

1. Professional Financial Experts

Every Mutual Fund scheme has a well-defined objective and behind every scheme, there is a dedicated team of financial experts working in tandem with specialized investment research team. These experts diligently and judiciously study companies, their products and performance, and after thorough analysis, they decide on the best investment option most aptly suited to achieve the schemes objective as well as investors financial goals.

2. Diversifying Risk

It plays a very big part in the success of any portfolio. Mutual funds invest in a broad range of securities. This limits investment risk by reducing the effect of a possible decline in the value of any one security. Mutual fund unit-holders can benefit from diversification techniques usually available only to investors wealthy enough to buy significant positions in a wide variety of securities.

3. Low Cost

Mutual Funds generally provide an opportunity to invest with fewer funds as compared to other avenues in the capital market. You can invest in a mutual fund with as little as Rs. 5,000 and also have the option of investing a little of Rs.500 every month in a SIP or Systematic Investment Plan.

4. Liquidity

You can encash your money from a mutual fund on immediate basis when compared with other forms of savings like the public provident fund or National Savings Scheme. You can withdraw or redeem money at the Net Asset Value related prices in the open-end schemes. In closed-end schemes, lock in period is mentioned, investor cannot redeem his investment until that period.

5. Variety of Investment

There is no shortage of variety when investing in mutual funds. There are funds that focus on blue-chip stocks, technology stocks, bonds or a mix of stocks and bonds and with due assistance from a financial expert, the investor can choose a scheme that aptly fits his requirements, and helps him achieve maximum profitability.

|

|

|

| |

| Types of Mutual Funds |

| |

1. Equity Funds

Equity funds aim to provide capital growth by investing in the shares of individual companies. Any dividends received by the fund can be reinvested by the fund manager to provide further growth or paid to investors. Both risk and returns are high but equity funds could be a good investment if you have a long-term perspective and can stay invested for at least five years.

2. Debt or Income Funds

The aim of debt or income funds is to provide you with a steady income. These funds generally invest in securities such as bonds, corporate debentures, government securities (gilts) and money market instruments. Opportunities for capital appreciation are limited.

3. Balanced Funds

The aim of balanced funds is to provide both growth and regular income as such schemes invest both in equities and fixed income securities in the proportion indicated in their offer documents. The investor may wish to balance his risk between various sectors such as asset size, income or growth. Therefore the fund is a balance between various attributes desired, however, NAVs of such funds are likely to be less volatile compared to pure equity funds

4. Liquid Funds

Liquid funds are a safe place to park your money; it is an appealing alternative to bank deposits because they aim to provide liquidity, capital preservation and slightly higher interest rates than bank accounts. Returns on these funds fluctuate much less compared to other funds as the fund manager invests in 'cash' assets such as treasury bills, certificates of deposit and commercial paper.

5. Index Funds

Index funds are passively managed funds i.e. the fund manager attempts to mirror the performance of a benchmark index like the BSE Sensex or the S&P CNX Nifty, by being invested in the same stocks. NAVs of such schemes would rise or fall in accordance with the rise or fall in the index.

Geographic Regions

1.Country or Region Funds

These funds invest in securities (equity and/or debt) of a specific country or region with an underlying belief that the chosen country or region is expected to deliver superior performance, which in turn will be favourable for the securities of that country. The returns on country fund are affected not only by the performance of the market where they are invested, but also by changes in the currency exchange rates.

2.Offshore Funds

These funds mobilise money from investors for the purpose of investment within as well as outside their home country. so we have seen that funds can be categorised based on tenor, investment philosophy, asset class, or geographic region. Now, let's get down to simplifying some jargon with the help of a few definitions, before getting into understanding the nitty-gritty of investing in mutual funds.

DEFINITIONS

Net Asset Value (NAV)

NAV is the sum total of all the assets of the mutual fund (at market price) less the liabilities (fund manager fees, audit fees, registration fees among others); divide this by the number of units and you get the NAV per unit of the mutual fund.

Standard Deviation (SD)

SD is the measure of risk taken by, or volatility borne by, the mutual fund. Mathematically speaking, SD tells us how much the values have deviated from the mean (average) of the values. SD measures by how much the investor could diverge from the average return either upwards or downwards. It highlights the element of risk associated with the fund.

Sharpe Ratio (SR)

SR is a measure developed to calculate risk-adjusted returns. It measures how much return you can expect over and above a certain risk-free rate (for example, the bank deposit rate), for every unit of risk (i.e. Standard Deviation) of the scheme. Statistically, the Sharpe Ratio is the difference between the annualised return (Ri) and the risk-free return (Rf) divided by the Standard Deviation (SD) during the specified period. Sharpe Ratio = (Ri-Rf)/SD. Higher the magnitude of the Sharpe Ratio, higher is the performance rating of the scheme.

Compounded Annual Growth Rate (CAGR)

What Does Compound Annual Growth Rate - CAGR Mean?

The year-over-year growth rate of an investment over a specified period of time.

The compound annual growth rate is calculated by taking the nth root of the total percentage growth rate, where n is the number of years in the period being considered.

This can be written as follows:

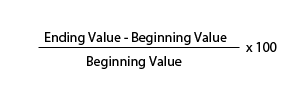

Absolute Returns

These are the simple returns, i.e. the returns that an asset achieves, from the day of its purchase to the day of its sale, regardless of how much time has elapsed in between. This measure looks at the appreciation or depreciation that an asset - usually a stock or a mutual fund - achieves over the given period of time. Mathematically it is calculated as under:

Generally returns for a period less than 1 year are expressed in an absolute form.

|

|

| |

|

|

|

|